Can freelancers get a mortgage in the UAE?

Yes, they can. But the application usually needs more preparation than a standard salaried mortgage file.

That is the part many freelancers do not realise at the beginning.

A salaried employee can usually show salary credits, payslips, and a salary certificate. A freelancer may have income from different clients, irregular payment dates, multiple currencies, project-based contracts, or business activity under a freelance permit or trade license.

That does not make mortgage approval impossible.

It simply means the bank needs a clearer story.

When I review a freelancer mortgage case, I do not only look at how much the person earns. I look at whether the income is easy for a bank to understand. Regular income, clean bank statements, low liabilities, strong savings, and proper documents can make a big difference.

In this guide, I will explain how mortgage for freelancers in UAE works, what banks usually check, which documents you may need, and how to improve your approval chances before applying.

Can Freelancers Get a Mortgage in the UAE?

Yes, freelancers can apply for a mortgage in the UAE if they meet the bank’s eligibility criteria.

The key point is income proof.

Banks want to see that your freelance income is stable enough to support monthly mortgage repayments. They may also want to understand your work activity, client payment history, bank statement pattern, credit score, debt burden ratio, and down payment source.

If you are a UAE resident with a valid freelance permit, trade license, residency visa, Emirates ID, and consistent income, your case may be possible.

If you are freelancing from outside the UAE and buying property here, your case may fall closer to a non resident mortgage in the UAE, depending on your residency, income source, and bank policy.

The right route depends on your profile.

That is why it helps to first understand the wider UAE mortgage options for different buyer profiles before choosing a lender or product.

Why Freelancer Mortgage Applications Need More Preparation

Freelancers are not always rejected because of low income.

Many are rejected because their income is not presented clearly.

For example, a freelancer may earn well, but the bank statement may show:

- Irregular client payments

- Cash deposits with no clear explanation

- Transfers from multiple personal accounts

- High credit card usage

- Business expenses mixed with personal spending

- Large income gaps between months

- No contracts or invoices to support client payments

- Unclear freelance permit or license status

From the freelancer’s side, the income may make sense.

From the bank’s side, it may look inconsistent.

That is the gap we need to close before applying.

A good freelancer mortgage file should answer three questions clearly:

Can you legally work as a freelancer?

Can your income be verified?

Can you repay the mortgage comfortably?

If the answer is clear, your application becomes easier to position with the right bank.

Freelancer Mortgage Eligibility in the UAE

Every bank has its own criteria, but most freelancer mortgage applications are assessed around similar factors.

| Eligibility Area | What Banks May Check |

|---|---|

| Residency status | UAE residence visa, Emirates ID, or non-resident status |

| Freelance activity | Freelance permit, trade license, or business registration |

| Income stability | Regular client payments, contracts, invoices, and bank credits |

| Income history | Usually several months of statements, sometimes longer depending on profile |

| Credit profile | AECB credit report, repayment history, existing credit cards and loans |

| Debt burden ratio | Whether your total monthly liabilities are within bank limits |

| Down payment | Source of funds, savings pattern, and available deposit |

| Property type | Ready property, off-plan property, residential unit, or investment property |

| Age and tenure | Whether the loan can finish before the bank’s maximum age limit |

| Bank appetite | Whether the bank accepts your type of freelance income |

The important point is this:

Freelancer mortgage approval is not only about income amount. It is about income quality.

A freelancer earning AED 40,000 per month with messy statements may face more difficulty than a freelancer earning less but showing clean, regular, well-documented income.

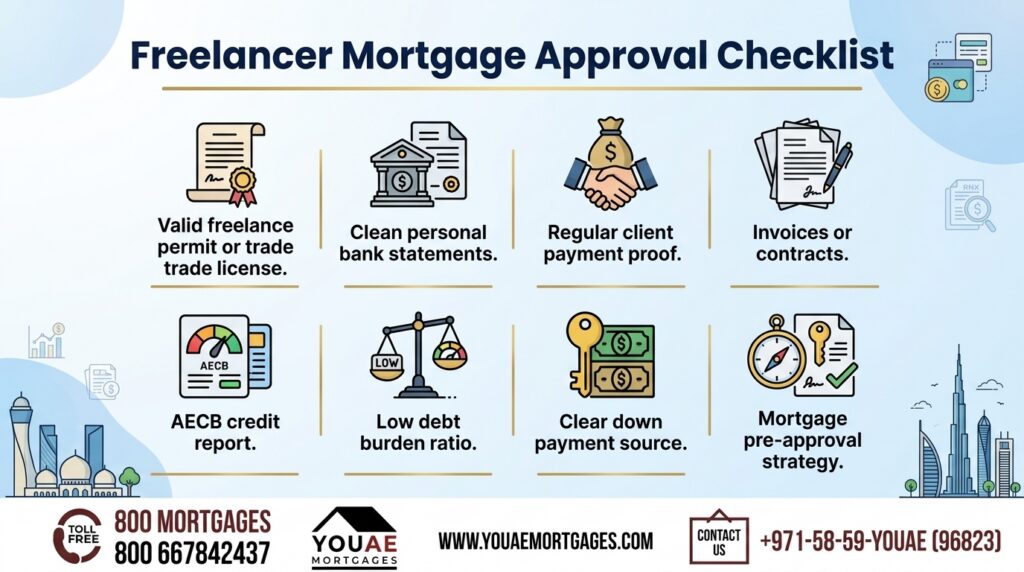

Documents Required for Freelancer Mortgage in UAE

The exact document list depends on the bank, but freelancers should usually prepare a stronger file than a salaried applicant.

Here is a practical checklist.

Personal Documents

- Passport copy

- UAE residence visa copy, if applicable

- Emirates ID copy

- Proof of current address

- Marriage certificate, if applying jointly with spouse

- Existing loan or credit card statements, if applicable

Freelance or Business Documents

- Freelance permit or trade license

- Free zone registration documents, if applicable

- Professional license or activity permit

- Client contracts, where available

- Recent invoices

- Payment confirmations from clients

- Business profile or summary of freelance activity

- VAT registration or returns, if applicable

Income Documents

- Personal bank statements

- Business bank statements, if you use a separate business account

- Proof of regular client payments

- Income summary for the last 6 to 12 months

- Audited financials, if available

- Accountant letter, if available and accepted by the bank

Property Documents

- Property details

- Sales agreement or booking form

- Title deed, if resale property

- Developer documents, if applicable

- Down payment proof

- Valuation documents, once required by the bank

For a wider document view, you can also review this home loan documentation checklist before preparing your file.

How Banks Assess Freelance Income

Banks usually want to convert your freelance income into a stable monthly figure.

That can be simple for salaried buyers, because the salary comes on a fixed date.

For freelancers, the bank may need to average income over time.

For example, they may look at:

- Total credits over a period

- Average monthly income

- Lowest income months

- Consistency of client payments

- Whether income is recurring or one-off

- Whether payments match invoices or contracts

- Whether the income is personal, business, local, or overseas

- Whether expenses reduce real affordability

This is why your bank statements matter so much.

If your income comes from three long-term clients every month, that is easier to explain.

If your income comes from random transfers with no invoices, no contracts, and unclear descriptions, the file becomes harder.

The bank is not only checking income.

It is checking predictability.

Why AECB Credit Score and DBR Matter for Freelancers

Freelancers should pay close attention to credit score and debt burden ratio.

Your AECB credit report helps banks understand how you manage credit cards, personal loans, car loans, and other liabilities. Late payments, high card usage, bounced payments, or too many recent credit applications can weaken your case.

Your debt burden ratio also matters because banks want to know how much of your monthly income is already committed to debts.

This can be especially important for freelancers because the bank may use an averaged income figure. If the bank uses a conservative income average and your liabilities are high, your borrowing capacity may be lower than expected.

Before applying, review how credit score and debt to income ratio affect mortgage approval. This is one of the most important preparation steps for any freelancer.

Bank Statement Tips for Freelancers Applying for a Mortgage

This is where freelancers can improve their mortgage file before applying.

Your bank statements should make your income easy to understand.

Here is what helps:

- Keep client payments traceable

- Avoid unnecessary cash deposits

- Separate personal and business activity where possible

- Keep invoices and contracts matching major credits

- Reduce overdraft-style behaviour

- Avoid returned payments

- Reduce high credit card balances

- Keep savings visible

- Avoid moving money through too many accounts without reason

- Explain large one-off transfers before the bank asks

If you are planning to apply for a mortgage in the next few months, start cleaning your statement pattern early.

A bank does not only see how much money came in.

It also sees how money moves.

For freelancers, clean account conduct can support the income story.

Mortgage Options That May Suit Freelancers in the UAE

Freelancers may qualify for different mortgage options depending on income, residency, property type, and bank policy.

Residential Mortgage

If you are buying a home to live in, a residential mortgage in the UAE is usually the first option to consider.

This may suit freelancers who are UAE residents and can show stable income, clean documents, and enough down payment.

Fixed Rate Mortgage

A fixed rate mortgage may suit freelancers who want predictable monthly payments.

When income is project-based or irregular, payment stability can be useful. A fixed rate can make budgeting easier during the fixed period.

You can compare the structure through this guide to fixed rate mortgages in the UAE.

Offset Mortgage

An offset mortgage may suit freelancers who keep strong savings.

Many freelancers receive larger client payments at different times of the year. If you keep some of that cash in savings, an offset structure may help reduce interest while keeping access to funds.

You can read this practical guide to offset mortgages in the UAE to understand how this type of structure works.

Islamic Home Finance

Some freelancers may prefer Shariah-compliant finance. In that case, Islamic home finance may be worth comparing with conventional mortgage options.

The right product depends on your preference, bank criteria, property, and total cost.

Non-Resident Mortgage

If you freelance outside the UAE and want to buy property here, your application may be treated as non-resident depending on your status.

In that case, the lender may look more closely at overseas income, foreign bank statements, country of residence, currency, and down payment.

Freelancer Mortgage Pre-Approval in UAE

Freelancers should try to get mortgage pre-approval before making a serious property offer.

Pre-approval helps you understand:

- How much you may be able to borrow

- Which banks may accept your freelance income

- What documents are missing

- Whether your DBR is comfortable

- Whether your credit profile needs improvement

- What deposit level may be required

- Whether the property budget is realistic

This is especially important for freelancers because approval can be more bank-specific.

One bank may accept your income structure.

Another may not.

That is why a pre-approval strategy matters.

If you apply randomly to multiple banks, you may waste time and create unnecessary credit checks. It is better to assess your file first, choose the right lenders, and apply with a complete document pack.

You can also review the step by step UAE mortgage approval process to understand how the journey works from eligibility review to final approval.

Common Reasons Freelancer Mortgage Applications Get Rejected

Freelancer applications are usually rejected for avoidable reasons.

The most common issues include:

- Income is not consistent enough

- Bank statements are difficult to understand

- Freelance permit or license is missing or expired

- Client payments cannot be verified

- Credit score is weak

- DBR is too high

- Down payment source is unclear

- Too many liabilities exist

- Business and personal funds are mixed without explanation

- Property does not meet bank criteria

- Applicant applies to the wrong bank

- Documents are incomplete

Many of these issues can be fixed before application.

That is why preparation matters.

If your case has already been declined, it does not always mean you cannot get a mortgage. It may mean the file needs to be restructured, documents need to be improved, or a more suitable bank needs to be selected.

This guide on common reasons banks reject mortgages can help you understand the bigger approval risks.

How Freelancers Can Improve Mortgage Approval Chances

Here is what I would suggest before applying.

1. Prepare Your Documents Early

Do not wait until you find a property.

Start collecting freelance permits, bank statements, invoices, contracts, credit report details, and down payment proof early.

2. Keep Income Easy to Trace

If a client pays you, make sure the payment can be connected to an invoice, contract, or regular work activity.

3. Reduce Unnecessary Liabilities

High credit card limits, personal loans, and car loans can reduce borrowing capacity.

4. Avoid New Loans Before Applying

Taking a new personal loan or car finance before mortgage application can weaken your DBR.

5. Keep Savings Visible

A strong savings pattern can help the file, especially if income is irregular.

6. Use the Right Bank Strategy

Not every bank views freelancer income the same way. Choosing the right lender can make a major difference.

7. Get a Broker Review Before Submission

A mortgage advisor can review the file before it reaches the bank. This helps identify weak points early.

For a broader preparation guide, read these tips to improve your mortgage approval chances.

Freelancer vs Self-Employed Mortgage in UAE

Freelancers and self-employed buyers are often grouped together, but they are not always the same from a bank’s point of view.

A self-employed buyer may own a company, hold a trade license, have staff, business accounts, audited financials, and company turnover.

A freelancer may work independently under a freelance permit, professional license, or free zone setup. Income may come from contracts, projects, retainers, or overseas clients.

The documents can overlap, but the file structure may be different.

That is why freelancers should not assume that generic self-employed advice is enough.

A freelancer mortgage file should explain:

- What work you do

- How long you have been doing it

- Who pays you

- How regularly payments arrive

- Which account receives income

- Whether income is local or overseas

- Whether the income can continue after mortgage approval

The clearer the story, the stronger the file.

Should Freelancers Apply Directly to Banks?

You can apply directly to banks, but freelancers should be careful.

Direct application works best when your income is simple, your documents are complete, your credit profile is strong, and you already know which bank accepts your profile.

If your income is irregular, multi-client, overseas, newly established, or difficult to document, direct application may be risky.

The problem is not only rejection.

The bigger issue is applying to the wrong bank first.

A mortgage broker can help compare bank appetite before submission. This is useful because banks do not all assess freelancer income in the same way.

At YOUAE Mortgages, the goal is to match the applicant with lenders that are more likely to understand the file, not just show a random list of rates.

If you are unsure where your profile fits, speaking with a UAE mortgage broker can save time and reduce avoidable mistakes.

Freelancer Mortgage Checklist Before Applying

Before you apply, check these points:

- Is your freelance permit or license valid?

- Do your bank statements show regular income?

- Can your client payments be explained?

- Do you have invoices, contracts, or work agreements?

- Is your credit report clean?

- Is your DBR under control?

- Do you have enough down payment?

- Is your property budget realistic?

- Have you avoided new loans or credit cards recently?

- Do you know which banks may accept your profile?

- Have you checked your monthly payment estimate?

You can use the UAE mortgage calculator to estimate payments before applying. The calculator will not confirm approval, but it can help you understand whether the monthly cost fits your income.

Final Thoughts

Freelancers can get a mortgage in the UAE, but the application needs to be prepared carefully.

The bank needs to see more than income.

It needs to see income stability, document clarity, clean account conduct, manageable liabilities, and a realistic property budget.

If you are freelancing and planning to buy property, do not wait until you find the perfect home before checking your mortgage position. Review your file early, clean up your statements, prepare your documents, and understand which banks may accept your profile.

A well-prepared freelancer mortgage application can be much stronger than a rushed one.

If you want to know whether your freelance income can support a mortgage, you can start your mortgage assessment with YOUAE Mortgages and get guidance based on your actual profile.

Frequently Asked Questions About Mortgages for Freelancers in the UAE

Can freelancers get a mortgage in the UAE?

Yes, freelancers can apply for a mortgage in the UAE if they can show valid identity documents, residency or non-resident status, income proof, bank statements, credit history, and enough down payment. Approval depends on bank policy and how clearly the income can be verified.

Do freelancers need a trade license to get a mortgage?

Some freelancers may use a freelance permit, professional license, or trade license depending on their setup. Banks usually want to see that the freelance activity is legal and properly documented.

How many months of bank statements do freelancers need?

Many banks ask for recent bank statements, often covering several months. Some cases may require longer income history, especially where income is irregular or self-employed-style documentation is needed.

Is freelance income accepted by UAE banks?

Freelance income may be accepted if it is regular, traceable, and supported by documents such as bank statements, invoices, contracts, permits, or licenses. Acceptance varies by bank.

Can freelancers get mortgage pre-approval in the UAE?

Yes, freelancers can apply for mortgage pre-approval. In fact, pre-approval is especially useful because it helps identify which banks may accept the income structure before the buyer commits to a property.

Is it harder for freelancers to get a mortgage than salaried employees?

It can be more document-heavy for freelancers because income is not always fixed or paid on a regular salary date. However, a well-prepared freelancer with strong income, clean statements, low liabilities, and proper documents may still qualify.

Can freelancers with overseas clients get a UAE mortgage?

Yes, but the bank may review the income source, currency, client history, foreign transfers, and statement consistency more carefully. If the applicant lives outside the UAE, the case may be assessed as a non-resident mortgage.

What mortgage type is best for freelancers?

There is no single best option. Some freelancers prefer fixed rate mortgages for predictable payments. Others may consider offset mortgages if they keep strong savings. The right option depends on income pattern, savings, risk comfort, and property goal.

Should freelancers take help from a mortgage broker?

A mortgage broker can be helpful for freelancers because bank appetite varies. A broker can review documents, identify suitable lenders, prepare the file, and reduce the chance of applying to the wrong bank.