Choosing the right mortgage product is one of the most important decisions you will make when buying residential property in the UAE. With different types of residential mortgage products fixed and variable available, understanding these mortgage options can save you time, money, and stress while supporting effective financial planning.

At YOUAE Mortgages, we work closely with leading UAE lenders who provide mortgages tailored to your needs. This guide explains the main types of residential mortgage products in the UAE in 2026, how they work, and when each option makes sense.

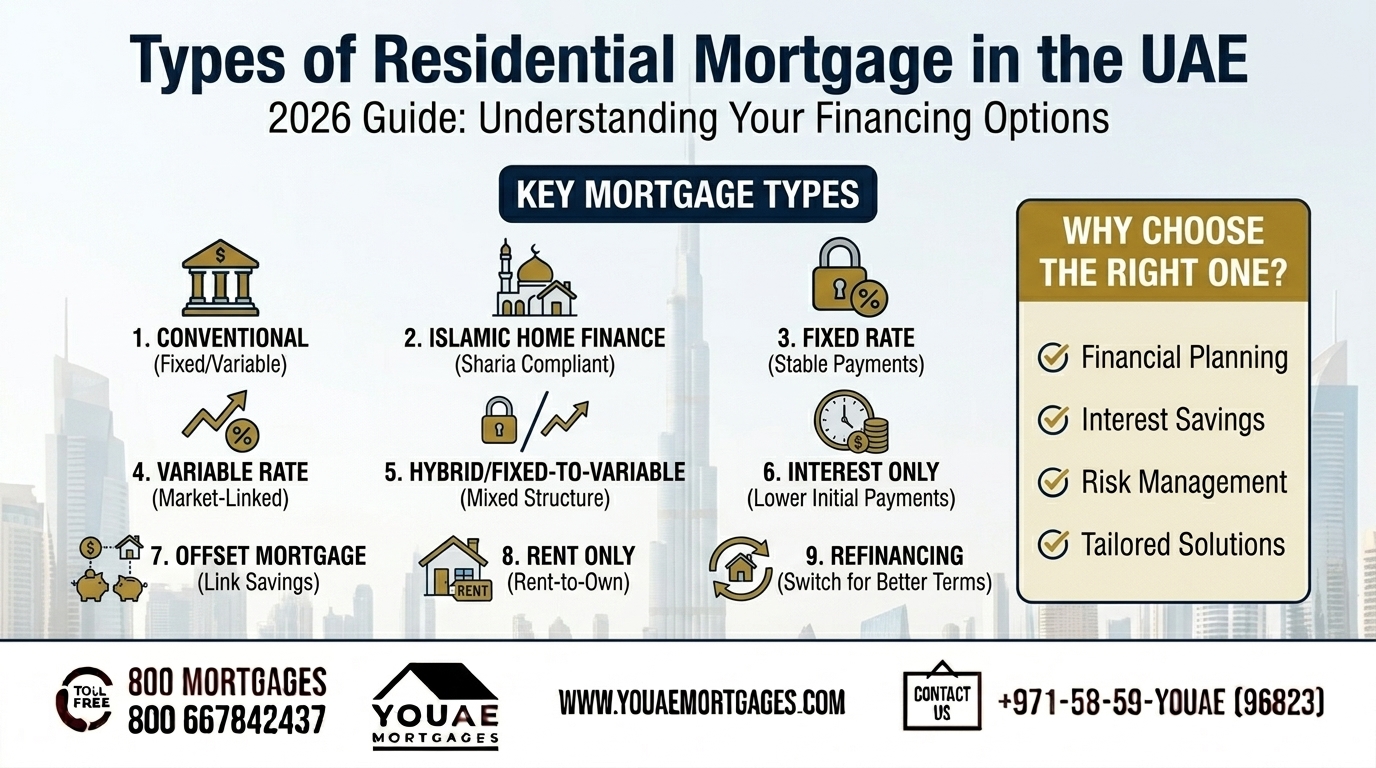

1. Conventional Residential Mortgages

Conventional mortgages are the most common types of mortgage loans in the UAE, typically ranging from 15 to 25 years in mortgage term. They are based on a traditional interest rate structure and are offered by most local and international banks.

How They Work ?

Banks lend a percentage of the property value, and borrowers repay the loan in monthly repayments comprising principal balance and interest. Interest rates can be fixed, variable interest rates, or a combination of both.

Who They Suit ?

Home buyers seeking predictable monthly payments or those comparing multiple lenders.

Key Features

- Predictable payment stability with fixed interest rate or flexibility with variable interest rates

- Options for fixed rate loans, variable interest rate mortgages, or hybrid rate structures

- Available for residents and eligible expats

- Mortgage interest rates linked to market conditions such as the emirates interbank offered rate (EIBOR) for variable rate mortgages

2. Islamic Home Finance

Islamic home finance products comply with Sharia principles. Instead of charging interest, banks use profit sharing or cost plus profit structures.

How They Work ?

Instead of lending money at interest, the bank may purchase the property and sell it to the buyer at a profit, or the bank and buyer may enter a partnership where profits are shared.

Who They Suit ?

Buyers who prefer Sharia compliant financing due to personal or religious preferences.

Key Features

- Interest free structure

- Sharia compliant contracts

- Often competitive pricing for eligible buyers

3. Fixed Rate Mortgages

A fixed rate mortgage locks the interest rate, ensuring that the interest rate remains constant for the entire term or a fixed loan period, typically ranging from one to five years.

How They Work ?

You pay the same monthly amount throughout the fixed period, regardless of interest rate fluctuations or market conditions. After the fixed term ends, rates may adjust based on interest rate movements.

Who They Suit ?

Buyers who value payment stability and want to protect themselves against interest rate fluctuations.

Key Features

- Predictable monthly payments ideal for financial planning

- Protection from market volatility and interest rate movements

- Provides payment stability throughout the loan period

4. Variable Rate Mortgages

Variable rate mortgages have interest rates that fluctuate based on benchmark rates, such as the emirates interbank offered rate (EIBOR), plus a bank margin.

How They Work ?

Your monthly repayments may increase or decrease as the benchmark rate changes with market conditions.

Who They Suit ?

Borrowers comfortable with some level of rate movement and who may benefit from periods of lower mortgage interest rates.

Key Features

- Potential for lower rates when the market falls

- Monthly repayments vary with interest rate movements

- Flexible but requires careful financial planning

5. Hybrid or Fixed-to-Variable Mortgages

Hybrid or fixed-to-variable mortgages combine features of both fixed and variable rate loans. The interest rate is fixed for an initial period before switching to a variable structure.

How They Work ?

For example, you may lock a fixed rate for the first three to five years, after which the loan switches to a variable rate tied to market benchmarks like EIBOR.

Who They Suit ?

Buyers who want initial payment stability followed by potential savings if mortgage interest rates decrease.

Key Features

- Short term payment stability

- Opportunity to benefit from interest rate fluctuations later

- Balanced risk and flexibility

6. Interest Only Mortgages

Interest only mortgages allow borrowers to pay only the interest portion for an agreed period instead of paying both principal and interest.

How They Work ?

Monthly payments during the interest only phase are lower because you are not paying down the principal balance. After this phase ends, payments typically increase as the principal must be repaid.

Who They Suit ?

Investors managing cash flow or buyers who expect higher future income.

Key Features

- Lower initial monthly repayments

- Higher future repayment amounts after interest only period

- Useful for specific financial strategies

7. Offset Mortgages

Offset mortgages link your savings account with your mortgage. Instead of earning interest on your savings, the bank offsets the savings balance against your mortgage balance.

How They Work ?

Savings reduce the amount on which interest is calculated, lowering the mortgage interest rates you pay and possibly shortening the mortgage term.

Who They Suit ?

Buyers with significant savings who want to reduce overall interest costs.

Key Features

- Reduces interest payable on the mortgage

- Encourages savings integration

- Can shorten loan period and reduce total interest

8. Rent Only Mortgages

Sometimes referred to as rent to own or rent first mortgage, these products allow buyers to pay rent for a period before transitioning into a full home loan.

How They Work ?

Instead of immediate home loan repayments, you pay rent for a defined period. Afterward, a mortgage is arranged for the property.

Who They Suit ?

Buyers who are not ready for immediate financing or need time to strengthen income or credit profiles.

Key Features

- Flexible transition from renting to ownership

- Time to improve eligibility and affordability

- Useful for first time buyers

9. Refinancing or Remortgage

Refinancing involves switching your current mortgage loan to another bank with better rates or terms.

How They Work ?

A new lender pays off your existing mortgage and issues a new mortgage, usually with better interest rates or repayment terms.

Who They Suit ?

Existing borrowers looking to reduce monthly payments or take advantage of lower mortgage interest rates.

Key Features

- Potential savings on interest

- Opportunity to restructure loan tenure or payment schedule

- May involve early settlement fees or transfer costs

Choosing the Right Type of Home Loan

Selecting the best mortgage product depends on your financial goals, risk tolerance, and long term plans.

Here’s how YOUAE Mortgages can help you choose with confidence:

- We assess your financial profile thoroughly

- We compare mortgage products from multiple lenders

- We explain each product type in clear terms

- We guide you through documentation and approval steps

- We help match you with the most suitable mortgage solution

After understanding the main mortgage types, it helps to compare which UAE mortgage option fits your buyer profile, especially if you are an expat, freelancer, investor, or non-resident buyer.

Final Thoughts

In 2026, home financing in the UAE offers a wide range of residential mortgage products to suit various needs. From traditional conventional loans to flexible hybrid options, each mortgage type has its advantages and ideal use cases.

Understanding these options empowers you to choose the right mortgage with confidence. For expert support Contact YOUAE Mortgages on 00971-58-59-96823 or write to us on info@youaemortgages.com, you can navigate the process smoothly and secure the home loan that best fits your financial goals and life plans.

People Also Ask

Which type of residential mortgage is best for first time buyers in the UAE?

Fixed rate or hybrid mortgages are often suitable for first time buyers because they offer predictable monthly payments and easier budgeting.

Can I switch my mortgage type after taking a home loan?

Yes, many banks allow borrowers to switch between mortgage types or refinance, subject to approval and applicable fees.

Are Islamic home finance products more expensive than conventional mortgages?

Islamic home finance is often competitively priced and in many cases comparable to conventional mortgage products.

Do all banks in the UAE offer the same mortgage products?

No, mortgage products vary by bank, and features such as interest rates, fees, and eligibility criteria can differ significantly.

Can I combine fixed and variable rates in one mortgage?

Yes, hybrid mortgages allow a fixed rate for an initial period followed by a variable rate structure.

Is an interest only mortgage risky?

Interest only mortgages can be useful for cash flow management but require careful planning due to higher repayments late

What mortgage product is best for property investors?

Variable rate or interest only mortgages are often preferred by investors, depending on cash flow and long term strategy.

Can non residents apply for residential mortgage products in the UAE?

Yes, non residents can apply, but available products and loan to value limits may be more restricted.

Are early settlement fees the same for all mortgage types?

Early settlement fees vary by bank but are regulated under UAE Central Bank guidelines.

Do mortgage rates differ for salaried and self employed applicants?

Rates may vary based on risk assessment, income stability, and documentation quality.

Is refinancing available for Islamic mortgages?

Yes, Islamic home finance products can also be refinanced or transferred to other banks.

Can I apply for multiple mortgage products at the same time?

You can explore multiple options, but submitting formal applications is best managed through a mortgage advisor to avoid credit impact.